The banking statistics offers enough of details to understand the phenomenon why Kashmir was restive over the JK Bank issue unlike other places, reports Masood Hussain

Last fortnight, when the governor Satya Prakash Malik’s State Administrative Council (SAC) resorted to a “flawed” decision-making on the Jammu and Kashmir Bank (JKB), it triggered a sort of a crisis. People from all walks of life were literally on the roads. People who do not understand the Kashmir economy better, might have been amazed by the response.

Post-demonetization, almost everything is now linked to banks as people are not expected to keep the money at home. Jammu and Kashmir’s entire market is being served by 2036 branches across 22 districts by 43 financial institutions. By the end of March 2018, the entire banking sector was holding Rs 109976.56 crore in their vaults, an increase by 9.74 percent against the March 2017 figure of Rs 99264.61 crore. What is interesting is that JKB alone was keeping Rs 68969.07 crore which makes 62.71 percent of the entire banking vault in the state. With 778 branches, it is interestingly, the JKB owns 38.21 percent of the entire branch network.

But banks are not supposed to park the savings of its clientele idle. They invest. Normally banks prefer the eco-system they work in. By the end of March 2018, the entire banking sector had cumulative advances of Rs 51914.29 crore. It means they have invested only 47.20 percent within the state of Jammu and Kashmir. The tally is slightly better than year 2017, when the credit-deposit ratio was 44.63 percent as the advances were at Rs 44305.66 crore. This means more than half of the deposits raised in the state are deployed outside the state. Reserve Bank of India (RBI), the banking regulator has set the benchmark of 60 percent.

JK Bank makes itself distinct by owning most of the loan book of the state. Its advances are at Rs 32068.89 crore. It means this bank alone controls 61 percent of the entire banking sector. Despite that JK Bank’s own CDR is low – 46.50 percent.

Jammu and Kashmir is a twin-capital state. They are the major economic centres generating a lot of business. In fact, the two cities own 52 percent of the entire banking vaults in the state. However, their credit worthiness is slowing down. By March 2018, Srinagar and Jammu would own only 41.93 percent of the overall credits from the banking sector. Jammu is better in savings while Srinagar is faster is credit appetite.

Jammu city has an elaborate branch network. Its 428 branches are more than double of Srinagar city, perhaps because its vaults are flush with money. By March 2018, total deposits were at Rs 36183.93 crore. Interestingly, the JK Bank had only 48.21 percent of it – Rs 17445.34 crore. But culturally, Jammu borrows less than Srinagar. Total advances in the city were at Rs 10987.15 crore only of which the JK Bank had a share of 40.13 percent only – Rs 4409.55 crore. The city is a chronic low CD ratio city where the banking sector invests only 25.28 percent of its deposit register, slightly more than one third of the benchmark.

However, the Jammu city has another chronic crisis. It is a high NPA city. Banking sector has 8.18 percent (Rs 898.29 crore) gone bad. It is literally the NPA capital of the state and a nightmare for the bankers.

Srinagar offers a counter view. In fiscal 2018, the entire deposit base of the city was only Rs 21725.6 crore. Of this, JK Bank alone had Rs 16799.85 crore in its vaults which is 77.32 percent. On the credit front, the total outstanding by the end of March was Rs 10781.19 crore of which JK Bank alone had a share of Rs 8769.24 crore which makes 81.33 percent of the entire loan book of the capital city. Srinagar has historically remained the main population exhibiting credit appetite. While the entire banking sector’s CD ratio is 49.62 percent, JK Bank’s CD ratio in Srinagar is 52.1 percent.

Srinagar has remained in crisis for last three decades. In fact, since 2008, it has been worse because of three summer unrests – 2008, 2010 and 2016, which have dented the capacity to do business as the existing businesses took the main hit. Then, in September 2014, came the historic flood that devastated the business. All the main business hubs in Srinagar were decimated from Sonawar, to Qamarwari including Lal Chowk, Karan Nagar, Rajbagh and Jawahar Nagar.

But the series of dents have not impacted the credibility of the market. Bank data suggests that it only has Rs 692.76 crore of assets in default which is 6.43 percent. Though second highest in the state, it still is better, in comparison to Jammu, a market that has no impact of the situation. Unlike Srinagar, Jammu functions six days a week, and there are no protest strikes.

If the data is analysed on regional basis, a completely different picture emerges. Jammu seemingly is more prosperous in comparison to Ladakh and Kashmir. By the end of March 2018, the banks were holding Rs 60772.97 crore. Of this, the state government owned JK Bank had access to only Rs 31193.84 crore which makes 51.32 percent of the entire deposits. It means, for half of the deposits, Jammu region would rely more on nationalised and private banks.

The story is almost safe if one sees the loan book: Of Rs 20042.27 crore that the entire banking sector has advanced in the region, Rs 10226.71 crore was advanced by the JK Bank. Its share in the regional loan book is only 51.02 percent. The low credit absorbing region – it has 32.98 percent of CD ratio, its overall deafly is 5.54 percent – Rs 1111.03 crore.

Ladakh region that comprises two scarcely populated Leh and Kargil districts has cumulative deposit vault of Rs 3848.86 crore of which only 55.52 percent is with JK Bank. However, in the Rs 1243.95 crore advances, JK Bank has a better share – 57.38 percent (Rs 713.8 crore). In region’s CD ratio, JK bank is better than all others. The defaults are quite low: 1.54 percent (only Rs 20.39 crore). However, what is interesting is that Leh economy is more than double of Kargil, thanks to the cash tourism economy.

Interestingly, Kashmir case is different than both the geographic regions. The overall deposit base of Kashmir is Rs 42470.48 crore and this is with all the banks put together. Of this, Rs 32753.75 crore is with JK Bank alone. It means, in Kashmir JK Bank has access to 77.12 percent of the entire deposit base.

When it comes to credit, the advances, the story gets all the more interesting. By March 2018, Kashmir had outstanding advances of Rs 26319.92 crore. In this, JK Bank has a share of Rs 20864.19 crore which makes 79.27 percent of the entire loan book. This makes Kashmir the capital of investment in the state because it has 61.97 percent CD ratio. In fact JK Bank has better: 63.7 percent in Kashmir. What makes it more attractive is that default is down – only Rs 1171.84 crore, which is only 4.45 percent. At one point of time, even after the 2008 unrest, the NPA percentage had gone down to less than one percent but it rebounded and appreciated because of the subsequent happenings that impacted the market.

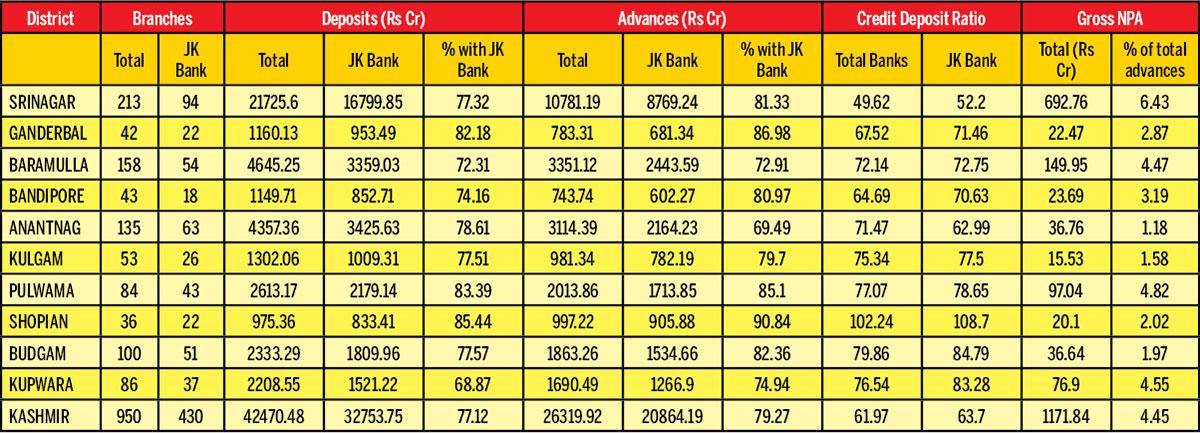

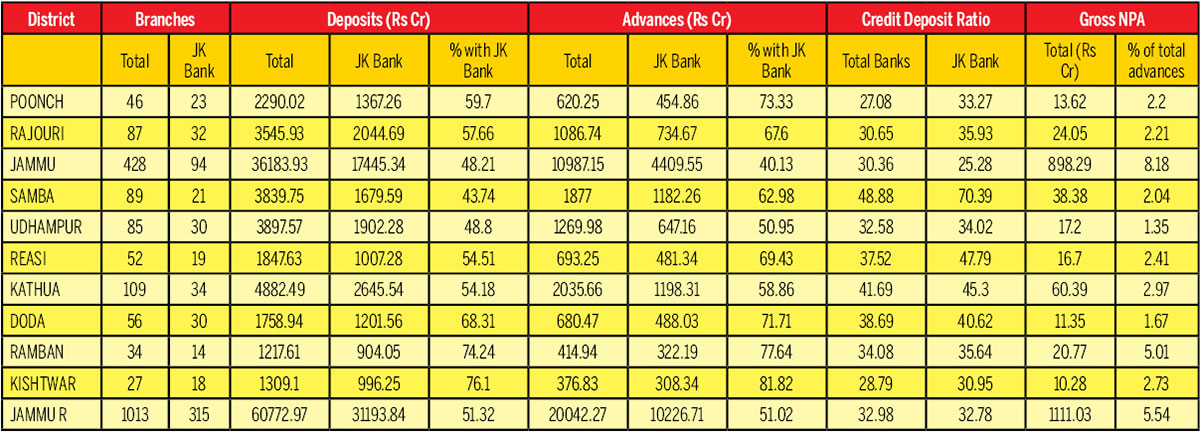

If the data is analysed on the district basis, a new trend emerges. There is no district in Kashmir that has less than 69 percent of its deposits with the JK Bank. It goes to the highest in 85.44 percent in case of Shopian. The same trend is exhibited by three Chenab Valley districts of Ramban, Kishtwar and Doda where the people keep their deposits with the JK Bank to the extent of 74, 76 and more than 68 percent, respectively. Even Kargil has reached a percentage of 69.62 percent in managing its deposits with JK Bank. Poonch and Rajouri trust JK Bank with their deposits to the tune of 59.7 and 57.66 percent respectively.

All other districts lag behind. At the maximum, they give JK Bank their deposits to in 43 to 54 percent. Rest of it is deposited with the nationalised and private banks.

By and large same story is seen on the credit front. South Kashmir Anantnag has the lowest share in the JK Bank advances – 69.49 percent. The highest is Shopian, the small apple district that has state’s highest CD ratio of 102.24 percent, which draws 90.84 percent from the JK Bank.

This statistics deconstructs why a particular demography was on roads when governor Malik resorted to controversial decision-making. The bank might have a pan-state existence and adequate shareholding amongst all regions of the state; it actually is a particular demography that has given it the trust and making it a success story of the state.