Crop insurance reached Kashmir five seasons after Jammu, covering 2.45 lakh farmers and collecting Rs 98 crore premium in 2023–24, but paid only Rs 31.66 crore in claims. Despite subsidised premiums and over Rs 362 crore collected since 2017–18, farmer reluctance, delayed settlements and apple exclusion hinder its effectiveness, writes Masood Hussain

With Kashmir emerging as the new crucible for climate change, shifting weather events are new villains for the farming community. They usually manifest as early snowfall in November or a massive heat wave in summer. Every time a crop fails, the crop insurance demand shrills.

Quite a few people know that the crop insurance landscape in Jammu and Kashmir has evolved significantly over the past seven years, growing from a limited initiative to a wide programme covering all 20 districts of the erstwhile state. This expansion, however, has not been without complications at the level of policymakers, farmers and even the insurance agencies. While enrolment numbers and premium collections have increased, the volume and consistency of claim settlements remain matters of concern, prompting scrutiny from farmers and legislators. But there is more to it than it

The scheme being implemented in the Union Territory is the Pradhan Mantri Fasal Bima Yojana (PMFBY), introduced across India in 2016. PMFBY was designed to offer financial protection to farmers against crop loss or damage resulting from unforeseen natural events, aiming to stabilise incomes and encourage continued agricultural activity even in the face of climatic uncertainty. “It is based on the yield,” a senior agriculture officer, who has been associated with the exercise for a long time, said. “If you have a consistent yield at the harvest at X, any reduction will get you right to a claim.” A huge quorum of insurance agents, agriculture and revenue officers usually for a crop-cut experiment once a season to decide the yield potential.

“There is another scheme as well,” the officer said, “While PMFBY provides comprehensive risk coverage from pre-sowing to post-harvest losses against non-preventable natural risks for the crops and notified areas, the RWBCIS provides indemnification for likely crop losses due to deviation in weather indices.” The second scheme operates differently. It knows the fixed weather parameters that help the crop have a better yield. “Any major shift in those parameters – humidity, temperature, rain- would make the farmer eligible for a claim because altered weather situation impacts the yield,” he added.

The premium structure of PMFBY is heavily subsidised. Farmers are required to pay only 2 per cent of the sum insured for Kharif crops and 1.5 per cent for Rabi crops. For commercial and horticultural crops, the farmer’s contribution rises to 5 per cent. The remaining premium burden is shared equally by the Central Government and the state administration. In principle, this makes crop insurance highly affordable. But in practice, delays in the disbursal of government subsidies to insurance companies have at times disrupted the claim settlement process, with many farmers facing long waits for compensation.

Jammu Kashmir Story

Soon after the scheme was devised by the central government, Jammu and Kashmir adopted it. An excited government offered a seven-crop basket for the scheme comprising paddy, wheat, maize, oilseeds, mangoes, saffron and apple. As the bids were invited, the insurers showed a keen interest in the Jammu plains, unlike Kashmir. In the subsequent years, they agreed to participate but backed off well before the negotiations could open. Third year, they agreed to look at oilseeds but were unwilling to look at the apple cart.

“It was frustrating but it was a learning curve,” one officer said. “Their reluctance to get into apple and saffron was because Kashmir has traditionally adopted anwaer system – eye estimation about the potential yield, which no insurer would agree to.” This frustration led the policymakers in Jammu and Kashmir to finally write to the government that the fruit basket should be delinked from the grains. It was active persuasion by the central government, especially after 2019, that the insurance companies started showing interest in Kashmir.

Gradual Roll Out

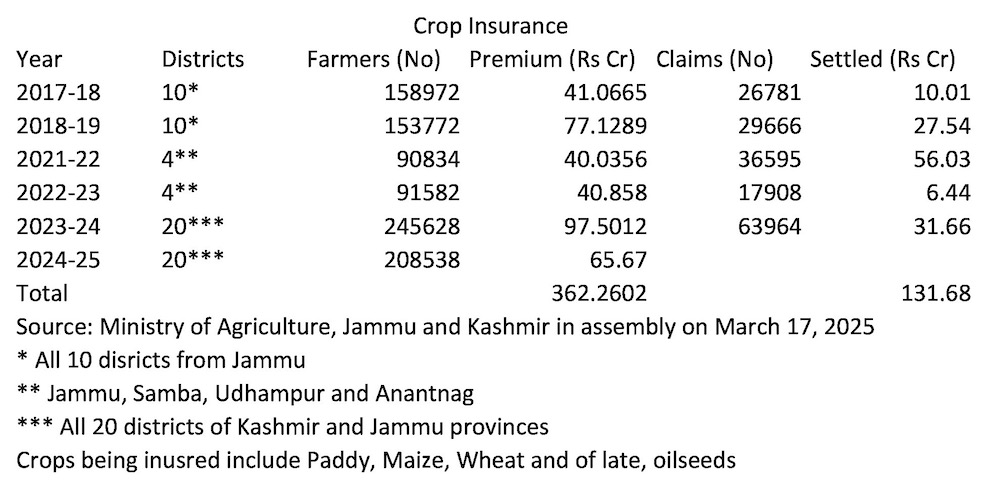

When the scheme was first launched in the region, PMFBY operated only in the ten districts of Jammu province. In the 2017–18 and 2018–19 crop seasons, enrolment averaged around 1.5 lakh farmers annually, and the combined premium collection for those years stood at Rs 118.2 crore. Claim settlements during that period, however, amounted to just Rs 37.55 crore, less than one-third of the total premiums. This gap between collection and compensation immediately raised questions about the scheme’s practical benefits.

A significant shift in the implementation pattern occurred in 2021–22, when four districts—Jammu, Samba, Udhampur and Anantnag—were included in the scheme. This was the first year in history when one of Kashmir’s 10 districts got a symbolic insurance converge. That year, enrolment dropped slightly to around 90,000 farmers, but the claim settlements reached a record Rs 56.03 crore, possibly indicating a season of acute crop loss or improved responsiveness from insurance companies. The following year saw similar enrolment and premium levels, but claim settlements fell sharply to just Rs 6.44 crore, despite over 17,000 claims filed. The reasons for this discrepancy have not been publicly clarified, but agriculture officials have cited variations in crop-cutting results and meteorological conditions.

In 2023–24, PMFBY was extended to all 20 districts of Jammu and Kashmir for the first time. Enrolment surged to over 2.45 lakh farmers, and the total premium collected approached Rs 98 crore. However, only Rs 31.66 crore was paid out in claims, once again reflecting a pattern where compensation remains disproportionately low compared to premium intake. For the ongoing 2024–25 season, 2.08 lakh farmers have enrolled and Rs 65.67 crore has been collected in premiums, though claim data is not yet available.

Cumulatively, between 2017–18 and 2024–25, over Rs 362 crore has been collected in premiums, while only Rs 131.68 crore has been disbursed in claims.

“If you calculate the overall inclusion of areas, Kashmir lost five cropping seasons as Jammu got eight,” the officer said. “The other interesting fact is that in the Kashmir region, the insurance is extended to oilseeds and paddy. Most of the rice fields have already been converted into apple orchards, and now farmers are reviving oilseeds, and in the last few years, the oilseed cultivation moved from 40 hectares to 140 hectares.”

The bulk of the crop insurance is extended to wheat that the Jammu plains cultivate in bulk. “If you see the overall cropped land that is covered under the scheme, it is barely 16 per cent. This is even though we are requesting the insurance agencies that they must take it to at least 25 per cent of the overall cropped area across Jammu and Kashmir”. Data presented in the parliament suggests that farmer number and the land remains low: 0.42 lakh hectares of 90834 farmers in 2021-22; 0.44 lakh hectares of 91582 farmers in 2022-23, and 1.25 lakh hectares of 245630 farmers in 2023-24.

Applecart

Kashmir’s key concern is the apple, as it remains the main driver of the peripheral economy. The crop insurance is always talked about when the fruit hits a weather crisis.

Officials said they had suggested to the government that fruits grown across Jammu and Kashmir may not be tackled under PMFBY because the traditional systems lack scientific methods in estimation, according to insurers. However, the suggestion is that fruits can be managed through the RWBCIS.

“After the farmers in Jammu started asking for insurance for mangoes and litchi, the files have started moving,” one insider said. “This year, we hope that the entire fruit basket will have insurance coverage.” The agriculture department has started the process, and the outcomes will be available soon.

Three-Year Contract

The positive part of the exercise is that once the bidding process completes, the agreements are signed for three years. “Now the government of India is planning to have one single process nationwide which will help in one-time decision-making by all states in one go for three years,” an insider informed. “We hope the pie improves so that the premiums get cheaper.”

Insurance companies selected through a bidding process implement the scheme district-wise. Firms that have operated in Jammu and Kashmir under PMFBY include the Agriculture Insurance Company of India, ICICI Lombard, IFFCO Tokio, Reliance General Insurance and Bajaj Allianz. These companies are required to sign agreements with the administration and financial institutions, with Jammu and Kashmir Bank serving as the nodal bank for implementation. There are almost 18 insurance companies which have agriculture insurance verticals, and this year, all have participated in the bids sought by the Jammu and Kashmir administration.

Reluctant Farmer

One major crisis that the officials pointed out is that the farmer is reluctant to seek insurance coverage. Since the produce is highly subsidised, the farmers’ share is less than Rs 100 a kanal but at times the peasantry backs out at the last moment. One officer said that farmers are weary of a lot of documentation that goes into the application process. Another officer said the farmers availing a loan must not have the right to opt out because it adds to their indebtedness in case of a crop failure.

“Between 2016-17 to 2023-24, which is eight years, the total farmer share in premium was Rs 55.92 crore,” the government said in the parliament. “The claims they made and were paid were Rs 127.66 crore.”

For loanee farmers—those who take seasonal crop loans (read Kissan Credit Card)—insurance is mandatory and is usually facilitated through their lending institution. Non-loanee farmers, who must enrol voluntarily, are often at a disadvantage due to a lack of awareness or limited access to official portals and Common Service Centres. In Jammu and Kashmir, the farming community is hugely indebted, and in case of crop failures, the debts surge further.

Farmers in Jammu and Kashmir are facing a mounting debt burden, with outstanding agricultural loans totalling Rs 17,814 crore as of March 31, 2024. Official data suggest that 9.29 lakh farmers owe Rs 16,481 crore to commercial banks, Rs 68 crore to cooperative banks and Rs 1265 crore to Regional Rural Banks. The average outstanding loan per agricultural household stands at Rs 30,435, according to the latest available data from the National Statistics Office (NSO). The survey, conducted by the Ministry of Statistics and Programme Implementation (MoSPI) in 2019, also found that 31.9 per cent of agricultural households in the region are in debt, a figure that highlights the financial distress among those dependent on farming.

That is perhaps why the concerned officials are keen that the KCC holders must have mandatory insurance cover. They believe that the inclusion of Apple will add numbers to a greater extent.

Officials deny that claims are delayed. “Under PMFBY during the last four years – 2020-21 to 2023-24, total claims of Rs 96.9 crore were made,” an insider said. “The fact is Rs 94.20 crore has been paid by January 1, 2025.” Lok Sabha was told that farmers in Jammu and Kashmir made claims worth Rs 124.34 crore between 2019-20 and 2023-24, and Rs 117.84 crore has been paid already.

However, there are reports about delays in the claim settlement process, which is hampered by other persistent issues. Many farmers complain about the lack of transparency in how losses are assessed, especially when crop-cutting experiments are conducted without their knowledge or participation. Remote sensing technology is increasingly being used for yield estimation, but this too has led to disputes, particularly in areas where actual crop conditions diverge from satellite-based assessments.

Dispute resolution mechanisms do exist, but their functioning remains inconsistent. District-level grievance redressal committees comprising officials, insurance representatives and farmer bodies are supposed to meet regularly, but in many areas, these forums are dormant. Farmers whose claims are rejected often find themselves without recourse, as escalation procedures to the State Nodal Officer or Ministry portals are rarely accessible to those in remote villages.

The administration, however, insists that the scheme remains essential for agricultural resilience, particularly in a region as environmentally fragile as Jammu and Kashmir. Officials maintain that digitisation, land record integration and mobile-based claim filing will gradually improve the system’s accountability and efficiency.

“The premium payment has three players – the farmer, the state government and the centre, the latter two sharing the major burden in equal proportion,” explained an officer. “The farmer’s share (though marginal) comes first, then the centre puts its share, but in states, there is a bit of delay. Unless the entire premium is paid, no claims are processed. But now things are changing. While the centre will pay its share upfront, with half of the state share, things will not move. This will revolutionise the system, and it is happening in a year or two.”

As the programme continues and more crops, such as oilseed, are brought under its purview, there is growing pressure on authorities to ensure that PMFBY evolves into more than just a statistical success. For the farmers of Jammu and Kashmir, the ultimate test of the scheme lies not in how many are enrolled or how much premium is collected, but in whether the compensation arrives when they need it most. It needs to operate like health insurance.