J&K’s only listed company, the Rs 100000 crore plus turnover J&K Bank turned 75 last week. While it has been at the core of money-management of individuals and institutions in the state for decades, R S Gull offers 10 distinct reasons about why the bank’s platinum jubilee is not an ordinary celebration.

Ageing is the only earthly constant. But how ageing impacts individuals and institutions differently was a key ingredient of the speeches that India’s Finance Minister P Chidambaram and Chief Minister Omar Abdullah delivered at the Platinum Jubilee celebrations of the J&K Bank, after the 80-pound cake carrying its logo baked at Lalit Palace was cut.

“Unlike human beings, when institutions age, they have the advantage of looking back at their successes and chart out its future,” Omar said. “Individuals will come and go but the life of institution if handled correctly is indefinite.”

“We become weak, weary, tired and need rest unlike institutions,” P Chidambaram said. “Institutions (react differently with ageing), they become stronger, take more responsibilities, reach out more people and face challenges.” He said he does not know who else will be around when the bank will complete its century in 2038. So he wished Kashmir’s biggest success story in advance.

But 75 years of J&K Bank is an amazing story. Its existence was not the desperation of the autocracy that (mis)ruled J&K. It was the public pressure that wanted freedom from moneylenders.

On the moneylenders’ front, there are only two historic references explaining resistance. The first was reported somewhere between 1900-1925 during Partap Singh era when a Robin Hood type resident Usman Chacha barged into the residence of the then major moneylender (Souder) of Kashmir, Ram Souder and stole away all his account books (khatas) from his Gurguri Mohalla residence and then tore it away and threw it into Jhelum in full public view.

The second instance was on October 1, 1938, when J&K Bank started operating despite stiff resistance to the idea by many influential people since 1920. The resistance was to the level that when Maharaja’s government sought help from the then banking experts Daya Krishan Kaul and Lala Hari Krishen, they rejected the idea asserting it was “impractical”. But history was finally created when the first branch started operating from Residency Road in July 1939. On day one, a cheque that came to the bank bounced. On day two, a loan of Rs 1.20 lakh was granted.

Defying the gravity that the political system offered for most of the state’s history of last 100 years, J&K Bank eventually emerged as a strong institution that is fundamental to the growth of state’s economy and a definition of the capabilities and capacities of J&K. Here are the 10 major reasons why Platinum Jubilee of J&K Bank is something that is not an ordinary celebration:

1. Institutional Resilience

The first crisis it suffered was when Mirpur and Muzaffarabad became the PaK and its assets (Rs 818742.4 annas) drowned, literally. Most of its clients who fled to Srinagar re-claimed their money they had deposited with the branches there. The situation became so acute that the emergency government then led by Sheikh Abdullah had to offer the bank a grant in aid of six lakh rupees in 1949. “But the bank that was strained on the liquidity front exhibited an impressive response,” said Chairman of CEO Mushtaq Ahmad. “Voluntarily, bank employees surrendered their salaries to manage the losses.”

Though the bank rarely suffered any loss later, there were occasions when margins dipped. These were apparent during the tensions on the borders – be in 1965 or later in 1971. Natural calamities especially the droughts had its impact, albeit temporary.

It was the rise of militancy in 1990 that was a major crisis. But credit goes to the bank that it converted it into an opportunity. As all the banks closed their shops and fled, it was J&K Bank that ran the show. With key players on the ground openly supportive of the change, the bank got a clean slate to start writing its success story. It reached its zenith in 2002 when it purchased the only surviving bank branch in Srinagar – the Grindlays, for Rs 2 crore, a year later after it had a corporate identity.

2. The Only Listed Company

Omar Abdullah did not hide his loss when he said he unnecessarily hurried in doing away with the maiden stocks he had purchased in 1998 when the bank went public almost a decade after its golden jubilee. “My first mistake was that I did not beg, borrow or steal to purchase as many shares as could have been possible when the bank went public,” Omar said. “My second mistake was when I sold the shares at a stage when the returns were in two-digits. Now I repent when I see the stocks being traded in four figures.”

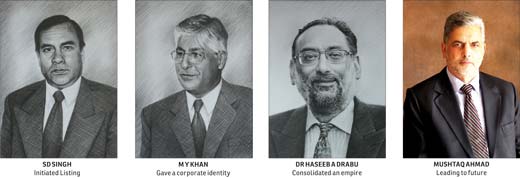

Credit must go to then-Chairman S D Singh (1992-96) who initiated the plan of going public. It was M Y Khan (1996-2003), his successor who created a movement for introducing the stock market to the masses. At the peak of militancy, he supervised a high decibel campaign that led to over-subscription of the issue. The Re 10 share crossed the psychological barrier of crossing Rs 1000 in January 2007.

While the listing at the BSE and NSE made the bank the only listed company, it introduced the stock market to Kashmir. Gradually scores of shops and stock investment companies started operating in Kashmir.

But the lone listed company of the state is subcontinent’s oldest surviving joint stock company. It falls under the old generation private sector bank now.

3. Only FII Magnet

Foreign Institutional Investors are a key capital source in listed companies and this bank currently has 27.11 percentage of its shares with the FIIs. It is one major parameter that speaks about the strong fundamentals of the bank. At one point of time, there were not a single Indian Institutional Investor in J&K Bank.

It took a few years after getting listed that the bank attracted FIIs. It was two in June 2000 and then it picked a year later. Right now there are 155 FIIs holding bank stocks. Of the 48477802 shares, right now 53.17% are with state government, 27.11% is with FIIs, 10.84% is with resident individuals, and the rest is with sundry corporate bodies, mutual funds, NRIs and Insurance companies.

4. Outsmarting The Master

J&K Bank has majority stakes with the J&K government. While the state government is doing away with its assets that it inherited from the autocracy, the bank has consistently increased its fixed assets – all in the last 25 years. Its latest was the formal launch of its National Business Centre (NBC) in Mumbai, the commercial hub of India. A nine-story complex offering around 50,000 sq ft space in one of the fashionable belts of Mumbai, this building made the bank J&K’s only institution that owns a high-rise.

“It has been our key priority that we must own enough of space for our operations and staff so that it gives confidence to all, the staff, the investors and the clientele,” says Chairman Mushtaq Ahmad. “We already have enough of our space in Delhi and other places.”

In Mumbai, the bank has 106 residential flats and at least a dozen branches are operating from the space it owns.

Same is true with Delhi. It owns a 4-story zonal office in Gurgaon, the new address of fashion and corporate, fetching it 55000 sq ft of space. Besides, it has 150 flats and at least three branches operating from the buildings it owns. “We have 37 flats in Bangalore, six in Chennai and eight in Kolkotta,” an officer associated with the upkeep of the fixed assets said. “This is in addition to the guest houses we operate in Mumbai and Delhi.”

Again, it is the only institution that has a huge presence across India. In February 1940, the bank started its operations outside the state with the first non-state branch being opened in Amritsar (shut in 1947 and reopened much later). And there was no looking back. By now, 111 of its 751 branches are operating outside the state and Chidambaram is keen to see the banks expanding outside J&K, even abroad.

5. Big Profit Maker, Huge Tax Payer

5. Big Profit Maker, Huge Tax Payer

Bank’s earning have tumbled a bit, given the fast-changing market situations, but never ever has it exhibited a loss. In the last fiscal, it earned a profit of Rs 1055 crore and for the current fiscal it is heading towards a Rs 1200 crore plus profit.

Though part of its profits goes to the corporate social responsibility, it has been the biggest taxpayer for the last many decades. “In the last fiscal, we paid an income tax of Rs 203 crore and for 2013-14, we have already paid Rs 265 crore,” Chairman Mushtaq Ahmad said.

6. The Last Resort Lender

That is where the strength of J&K lies. Historically, J&K has had an intense credit appetite but it was systematically denied by the system. But the rise of the state’s own bank has helped manage most of the credit requirements in the state.

By the end of June 2013 when J&K market was serviced by 1656 branches of 42 banks and financial institutions with access to Rs 64627 crore deposits, the overall credit offtake outstanding within the state was Rs 25461 crore excluding Rs 649 crore in state securities. The share of J&K Bank in the overall outstanding credit is Rs16943 crore which is 66% of the total corps. The big baddies of the banking continue to be conservative – SBI has only 9% stakes and PNB has 3%.

The priority sector credit outstanding in the state is of the order of Rs 14704 crore and J&K Bank alone has a share of Rs 9095 crore which is 61% of the total. By and large, most of the entrepreneurial and self-employment schemes would fall flat in absence of J&K Bank.

7. Model Employer

At the peak of militancy when survival was the first priority, it never gave up its systems and discipline. Barring exceptionally grave situations, its business units opened and closed in time. Even at the peak of 2008 Amarnath land row when both Jammu and Kashmir were closed for most of the summer and later in 2010 that crippled Kashmir for most of the year, nobody faced a liquidity crisis: thanks to ATMs that bank employees would fill during nights.

As its operations are expanding, its requirement for human resources is increasing. Right now, it is the main employer of management and business graduates. After the state government, it is J&K’s second major employer. With 10097 people on its rolls at all ranks as on date, by the way, it is the big daddy in the banking sector as far as an employer of Muslim minority is concerned. There is no bank in India that employs such a large number of Muslims, simply because it is owned by a state government that has Muslims a dominant demography.

Its Muslim majority status was key to an idea that was discussed, once in the PMO: why this bank cannot be encouraged enough to expand in Indian plains where ‘un-bankable Muslims live? The idea was mooted at some level in the policymaking in the backdrop of the Justice (retired) Rajinder Sacher report that identified massive grey areas in the access to basic facilities to Muslim minorities in India. Prime motivation was that homogeneity of faith and culture will help in their financial inclusion. Nobody knows where the file has gone!

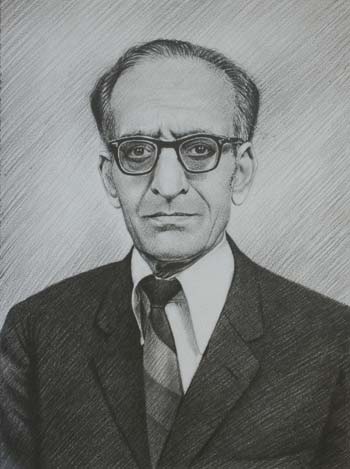

While its staff has been investing its blood and sweat, the management has not been completely ignoring their contributions. While the state employees are struggling to get their age of superannuation extended to 60, J&K Bank has already done it during the reign of Dr Haseeb Drabu, in whose era the FI witnessed a massive organizational re-structuring.

8. Explaining Capacity

Generally, J&K Bank is considered to be an expression of what is possible in a state like J&K that is small in size, has narrow and scattered resources, diverse and heterogeneous demography and which is at the periphery of the market and trendy incubations and practices. Even Chidambaram talked in details about keeping pace with the technology that is evolving and changing every other day. He even suggested that he can help the bank in deploying its personnel with bigger banks so that they get adequately trained.

But the bank that introduced the plastic money to Kashmir is consistently evolving to match the market competition. Banks with centralized systems and banking are offering nothing more than what this state-owned bank offers.

It goes to the credit of the bank that, despite problems in the overall market, situations and the priorities, it has emerged a strong bank. “All our parameters are best and indicative of the fundamental strength we have,” Mushtaq said. “We are the least NPA bank in India.” Even the Finance Minister praised its strong parameters.

The beauty of creating this success story is essentially a phenomenon of the last less than 25 years when the situation was bad, full of challenges and circumstances were trying at all fronts. In his platinum jubilee speech, Mushtaq stated: “In our Silver Jubilee year (1963) our annual business turnover was Rs 5.79 crore and the profits of Rs 2.47 lakhs. In the Golden Jubilee year (1988) business turnover had improved to Rs 1227 crore and profit to Rs 1.49 crore. Today in our Platinum Jubilee year, we have crossed a business turnover of Rs one lakh crore as the profits have crossed Rs 1000 crore.”

During the years of turmoil, the bank actually became a specialist in conflict banking – a rare feat that no other bank in India has, right now. Managing technology upgrades, introducing innovative products, battling modern moneylenders (in the apple trade) and ensuring recoveries during a life-threatening era is something that no other contemporary FI can claim. It was this cutting edge performance that led the Government of India to ask J&K Bank to implement the community information centre (CIC) scheme that J&K knows as Khidmat Centres.

9. Only State-Owned Bank

Most of the banks that emerged in India prior and post-partition were nationalized. J&K Bank is the only commercial bank that is still owned by a state government. Various states do own small cooperative and rural banks but no commercial bank is with any state, right now. This gives it a different identity, something that people would like to retain forever.

10. Banking A State

J&K bank has the distinction of being the only commercial bank that is conducting the treasury operations of any government in India. It has been the debt manager of the state government for 73 years until Omar Abdullah government decided to do away with the system and avail the ways and means exit from April 2011. The state government availed a one time grant of the RBI that helped it manage J&K Bank’s overdraft liabilities forever.

The state government has been explaining its wisdom for its decision for all these years including the Platinum Jubilee event. While bank’s only problem was to deploy the resources that came to it all of a sudden and lost one of its most credible bulk credit users, it was the state government that lost much. Under the ways and means, the state government is supposed to follow a strict system of supply and demand, something which was very flexible with J&K Bank in between.

As a regulator and the central bank, RBI is taking care of the official businesses of all the states (at least 18) excepting the J&K. With this, J&K government has lost a claim that it enjoys a special position on its fiscal management within India. Now it is as good as all other states. The state planners had argued that its outgo on interest will reduce by managing the OD but it has only increased!

After the agreement, however, RBI signed a separate agreement with the J&K Bank appointing it as its agent for conducting the general banking business of the state government. Even this offers another distinction to J&K Bank: right now, it is the only commercial bank that is authorized to conduct central bank business in J&K.