As Amitava Chatterjee, the second SBI banker, takes over as the new honcho of the Jammu and Kashmir Bank (JKB) post-2019, he steps into a market brimming with potential. The dominant banking institution in the erstwhile state of Jammu and Kashmir, JK Bank offers a captive market with surplus funds and high credit demand from the resurgent businesses gasping for credit lines and particularly from the large pool of unemployed youth, bubbling with ideas. This unique opportunity allows him to experiment with bold strategies. However, he must overcome a series of significant challenges first, writes Masood Hussain

In Amitava Chatterjee, the Jammu and Kashmir Bank (JKB) has a CEO who is a seasoned banker and has had a long career at the State Bank of India (SBI), the major bank in India. He succeeded Baldev Prakash, who also came from the SBI’s technology vertical to lead the bank. Chatterjee was heading SBI Caps, the premier bank’s investment banking subsidiary.

“I feel honoured to lead JK Bank, an institution with a rich legacy of trust and excellence,” Chatterjee was quoted as having said after taking over. “I am eager to collaborate with the talented team here to build on the strong foundation and drive the Bank’s vision of financial empowerment, sustainable growth, and innovation.”

In Jammu and Kashmir, JKB is the key builder of the economy and the main mover and shaker in the finance market. It has a history as being the lender of last resort for both the Jammu and Kashmir government and the commoner on the street, a capacity that was dented of late. It is the main deposit vault and the lone player in the sector, the distribution of even whose wall calendar can trigger a law and order situation. Shareholding apart, people have immersive emotional equity in the Bank.

In the last slightly more than half a decade, the bank skipped its banking style, which it had evolved over the decades of working in a culture. It gave up emotion to pave the way for strait-jacketed impersonal processes. It sounded political if not politicised. This made it distant and robotic. Chatterjee, as a well-meaning banker, has hinted at consolidating the gains and taking it to the next level. His team is upbeat with whatever he has talked about in very limited interactions so far. However, before he gets into steering one of the oldest surviving banks in India, Chatterjee may have to take note of the challenges that he faces right now.

Sluggish Topline Growth

Regardless of the claims made from high pedestals that JKB was retrieved from sinking at the last moment, the larger reality is that financial institutions make profits and book losses because they are in business. The losses cannot always be attributed to the erosion of the fundamentals but earmarking of adequate resources to fund provisioning requirements against bad debts. There were at least three occasions in recent years when the JKB booked losses, which coincided with the superannuation of MY Khan, Mushtaq Ahmad and Parvez Ahmad. These losses helped the institution have a cleansed balance sheet and in the improvement of its key parameters.

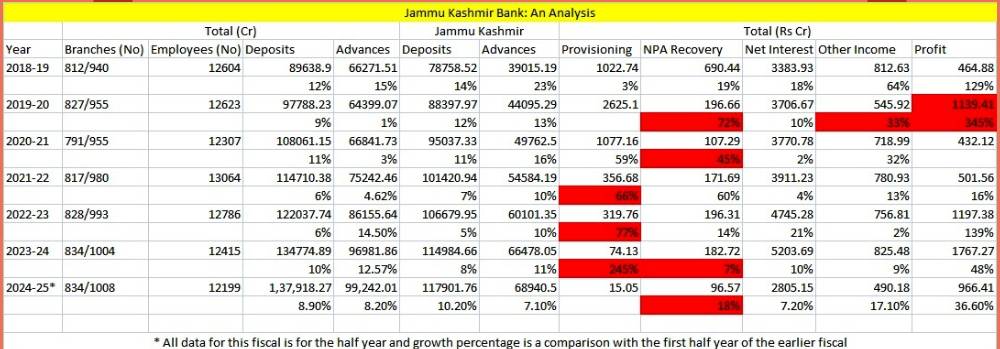

Unlike the past, however, what is worrying the insiders is that the bank’s topline growth has been sluggish in the past few years despite stable political conditions and a resurgent market. The primary income that banks make is from earning interest for themselves and their depositors.

Sluggish apart, it is too fluctuating (see table). From 18 per cent in 2018-19 to 10 per cent in 2019-20, two per cent in 2020-21, four per cent in 2021-22 and finally 21 per cent in 2022-23 and 10 per cent in the last fiscal, the growth in the net interest income of the bank has been dismally low both by market standards as well as its own previous benchmarks.

The decline in the topline growth is indicative that the Bank has given up its fundamental activity—lending, including priority sector lending. This could either be a credit demand issue or a pathetic reluctance to lend. While the credit demand should have apparently gone up because of stable market conditions, the reluctance to lend seems to be the dampener.

In such a situation if a financial institution is still showing profits, it means its non-core operations are too robust or it is showing off the family silver – unclogged funds parked elsewhere. In between the two is the story behind the profits that were claimed to be the outcome of post-2019 interventions.

Apart from the interest-earning and the non-interest income – mostly insurance and commission, one banker explained, that the profits are driven from the release of funds set aside for provisioning and recovering the outstanding.

At the peak of the crisis (2019-20), the bank had set aside Rs 2625 crore for provisioning, the requirement of which has gone down to Rs 74 crore in 2023-24. Not much is being lent, he said, asserting this is getting the bank into harm’s way. Chatterjee may have to work on the topline curve since he does not have the luxury of less provisioning, an opportunity his predecessor milked relentlessly.

Eroded Market Share

In June 2019, when the then Chief Secretary, BR Subramanian presided over the last meeting of the bankers operating in Jammu and Kashmir state, the Prime Minister’s confidante did ask about particular figures about their operations in Kashmir. Then, JKB held 39.28 per cent of the branch network in Jammu and Kashmir, 63.09 per cent of the entire deposits and 69.32 per cent of the loan book, the bank’s milch cow.

In June 2019, when the then Chief Secretary, BR Subramanian presided over the last meeting of the bankers operating in Jammu and Kashmir state, the Prime Minister’s confidante did ask about particular figures about their operations in Kashmir. Then, JKB held 39.28 per cent of the branch network in Jammu and Kashmir, 63.09 per cent of the entire deposits and 69.32 per cent of the loan book, the bank’s milch cow.

In September 2024, when the bankers of the Union Territory met for the UTLBC meeting, the JKB’s branch network had dwindled to 38.59 per cent, deposits to 62.52 per cent and the advances to 57.65 per cent – a more than 12 per cent fall in the bank’s share in the overall loan book.

Some bankers within JKB attribute it to ‘market forces’ and justify it by asserting that part of the operations were separated as Ladakh moved out as a separate UT. Even if Ladakh’s entire banking business is added to that of Jammu and Kashmir – as it used to be, JKB’s branch network goes down further to 37.46 per cent, deposits to 62.33 per cent and loan book bleeds further as its advances share reaches 57.55 per cent.

The growth of deposits and the advances continued falling. The bank’s loan book grew by an impressive 15 per cent in the last year when Jammu and Kashmir was a state. It fell to one per cent in 2019-20, three per cent in 2020-21, and 4.62 per cent in 2021-22 and finally improved to 14 and 12 per cent for the next two fiscals, respectively. The deposit growth in the last three financial years is between seven and eight per cent with 2022-23 even showing only five per cent growth. It essentially means the bank’s core business is not growing especially in the market that has traditionally been loyal to it and where it commanded an overarching reach not so long ago.

How and why did it happen is a question for analysts, investors and history alike. However, Chatterjee has all the ways and means – besides the team, to undo it and recover the market share it once had.

Unhappy Clientele

Jammu and Kashmir, more specifically Kashmir has passed through a situation for decades in which trade and business activities became the principal targets. Since 1990, there have been curfews and strikes for nearly 2000 days. Experts believe that the survival of formal businesses in this situation is exceptional and may be part of the resilience that trade has exhibited. Post 2019, there were no strikes – barring after August 2019 and later COVID-19, but the trade could not flourish because it had legacy issues linked to the twin unrests in 2010 and 2016 and a devastating flood in 2014.

Unlike in the past, when elected governments were mindful of these ground realities, the post-2019 systems, both within and outside the bank, failed to take these issues into account. There were certain issues which could have been tackled at the bank level. However, a huge narrative emerged that the Kashmir businesses were the outcome of the fraud and special dispensations. The changes in the industrial policy emerged as a major game-changer and started impacting the established manufacturing set-up. The invoking of the SARFESI law added to the crisis.

Debts getting bad is a normal banking routine and recoveries and restructuring are the possible options within the means and systems as long as intentions are clear between the two sides. However, the process of debt recovery employed in recent years became a major disruptor that impacted the reputation of individuals, their business concerns and, in certain cases, their homes. Industry associations went public with instances of the bank attaching collaterals worth crores for NPAs of lakhs of rupees.

“In fiscal 2018-19, we recovered Rs 690 crore of NPA without making a fuss of it. In 2019-20, the NPA recovery was Rs 196 crore,” one erstwhile banker, who served JK Bank, said. “In last four and a half years, the NPA recovery was not more than Rs 700 crore, still there was a lot of unwanted noise.” In the corporate world, companies dislike pandemonium especially when it surrounds them.

A businessman disposed of his huge property to repay the debt even though it was not bad. “It was reputation at stake. The fear was if things get bad, what they will do,” the businessman, talking anonymously, said. “Thank God, I managed it. I now work with a different bank.”

Business in uncertain times is more about risk and less about profit. Most of the businesses in Jammu and Kashmir are debt-funded. As the tensions hovered around, people stopped thinking of risk and consolidated and avoided expansion. This impacted the job market too.

Chatterjee may require investing his time and efforts in restoring the potential native investors’ lost confidence by doing away with strong-arm tactics. Jammu and Kashmir Bank’s 71 per cent loan book is spread over erstwhile Jammu and Kashmir and the credit in Jammu and Kashmir is expensive in comparison to other states.

Government Policy

For the Jammu and Kashmir government, the JKB has always been a jewel in its crown. It has been its own baby as the government is the majority shareholder of the bank. It still is the main agency for managing the government’s debts and loans and the main courier for implementing state-sponsored schemes. Of late, however, the situation seems to have changed.

Earlier, every government department had to open an account in the JKB and most of the transactions would take place through the bank. Not anymore. With the Ministry of Home Affairs (MHA) taking over the salary component of the Jammu and Kashmir Police (JKP), the second most populous department of the erstwhile state, all the transactions have shifted to the State Bank of India (SBI).

Now the government departments are bargaining with banks officially on deposits and park it where they get more. The most interesting is that the Jammu and Kashmir Wakf Board has also migrated from JKB to HDFC Bank.

This situation is adding to the tensions that the JKB is facing. It is no longer the most preferred bank for the Jammu and Kashmir government.

More importantly, the Bank is being managed by the government bank like one of its departments ignoring the fact that the bank has a separate corporate identity, whose affairs have to be managed by the Board in which the government has adequate representation. This has dented the commercial interests of the Bank as it is being dragged to be the delivery department of numerous welfare schemes of the Government.

“Since the Government is more interested in numbers and pressures the Bank to achieve them at any cost, the due diligence in delivering the government-led credit schemes has gone for a toss”, said one former banker privy to the developments.

Unhappy Staff

Last three years, the staffers in the bank said they are a scared lot. The tensions have gone to a level that staffers in good numbers are leaving the premier financial institution. It includes at least two DGM-level officers in the last two years

Off late, the bank opened for lateral appointments getting in professionals from other organisations to manage a staff that had evolved its own algebra of business, without compromising the core banking. One particular order that has hugely impacted the advances’ growth pertains to the assessment of lending officers’ wisdom in case a loan goes bad at any point in time.

“What is the logic for this?” an erstwhile banker said. “A bank is like a shop. You make a profit and sometimes you book a loss. Why should my employer judge me by an unintentional loss ignoring the gains I have had over my career?”

There were certain cases in which some employees were punished at the far end of their careers. It had a cascading impact and the loan managers are too cautious in lending now.

Cases, not so harsh though, were earlier in the bank too. Then, the staff would see the Board of Directors or convey and it would get comprehensively examined. The post-2019 board is non-native and they, according to insiders, fly with their ideas for implementation. “They see the bank as a machine and not as an institution that is rooted in the socio-economic life of Jammu and Kashmir,” one officer said. “We rarely have access and by and large the Board is hardly interested in knowing about the credit requirements and the business culture in Kashmir and Jammu.”

Earlier, the Board would have the best experts from the field and native components too. While one side would get the best practices from the market, another side would locate the significance of these interventions in Jammu and Kashmir. Now the Board has a young college teacher on its board whose selection came based on a paper she had written as part of her academics.

Soon after 2019, the new bank management started copying the traditional SBI model. The private sector architecture was undone and the PSU bank style was reinforced. Of the three MDs post-2019, two came from SBI including the incumbent.

“Our bank has its own uniqueness that honchos from SBI may not appreciate,” one banker said. “But it does frustrate especially because they do not understand or want to understand that employees in our bank have the same emotional equity in the institution that the society has.”

Technology Deficit

When SBI’s technology leader Baldev Prakash joined the bank as the Managing Director and CEO replacing the Chairman and CEO, RK Chibber, who moved on to become a trustee and Treasurer in VHP (Global), an impression in the JKB was that the bank’s technology platform will emerge matchless. That, however, was not to happen as he had different priorities and on the two succeeding Eid festivals, the bank’s most popular app reported massive outages.

Right now, most of the banking is technology-centric. Technology has taken centre stage in banking after the government’s sustained focus on digitalising financial services. Banks are investing massively in technology hardware and software. However, JKB has traditionally been on the wrong side of the digital divide even though it has pioneered in getting banking-related technology home.

Interestingly, Jammu and Kashmir has massive cell phone penetration and has almost 98 per cent financial inclusion, credit goes to JKB. A tech-weak bank is preventing the better use of the money for the people.

The world is gradually inching towards a situation in which the formal banking system will compete with lending apps that youngsters in society will develop. The cell phone has emerged the wallet and the vault. Banks are increasingly deploying artificial intelligence to reduce costs, make predictions to hedge risk, improve output, and get new businesses.

Though not visible, the JKB is facing a lot of competition from fin-tech. With NBFCs tying up with fin-techs and eating almost all the consumer finance pie, the out-of-date practices of JKB are not standing the test of time and resulting in poor credit growth in the consumer finance segment. Right now, when people go to make white goods purchases, they get instant financing from various fin-tech companies and JKB is nowhere in sight.

Chatterjee needs to generate a futuristic vision and adopt it for gradual implementation. He will have to create resources to deploy for this capital-intensive intervention. Now the survival of banks hinges upon how they adopt technology. The bank needs to have the vision to see that, the will to spend on technology and most importantly the resources to invest in high-cost technology interventions to stay ahead of their competitors.

Turbulent Scenarios

After Industrial Revolution IV, Jammu and Kashmir is a small space but part of a large global village. A technology shift in Silicon Valley has a global impact. The disturbed Middle East and the Ukraine War have already impacted this part of the world as no insulations exist. As the world order is gradually shifting towards a new Cold War, India for the first time is expected to be the theatre of many future events, especially because it has a huge emerging economy.

To steer clear of the headwinds, the managers at JKB, the only major listed company in Jammu Kashmir, under the new CEO’s leadership are expected to have a vision to sustain the status in a highly fragile market and ensure growth.